OFfshore Property Investment - Not for the Faint-hearted.

by Matthew Campaigne-Scott

Timing is everything, and if it isn’t then learning from history is. Continuing to make the same offshore property investment bungles could be the result of a combination of emotional frustration, Afro-pessimism and a Moby Dick like obsession with the Rand.

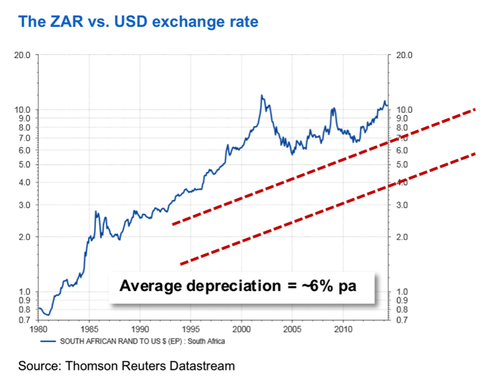

In 1997 the South African government allowed its citizens to take R200 000 per capita per annum to invest offshore. One may argue that investors practically ran to the offshore hills from an outperformed JSE and evaporating Rand. South African investors stood clutching their modest handful of Rands and looked up in wonder at a booming Wall Street. By 2001 the rand had fallen to R13.50 to the Dollar.

Who would believe that ten years later many countries would be on the verge of bankruptcy and that people would be grumbling about the “Strong Rand” and that the South African Equity market had outperformed most other markets over the same period?

But those in this game for the long haul will remind us that when all seems lost, it’s time to role up the sleeves and capitalise. Back in 2001 when fear gripped investors it was actually the right time to buy into SA equities. When the rand collapsed and afropessimism crept in, investors bought Dollars and Euros expensively and sold out of arguably undervalued markets and bought into markets trading at large premiums.

Looking back over ten years, comparisons have been made to a R100 investment in the JSE all-share index at the end of 2001 that would have been worth about R400 by the end of June this year, versus only around R94 if invested in the MSCI world index over the same period. The main US equity index, the S&P500, is today still roughly 10% below its peak in 2000 in rand terms. Emotions have been the main driver of the investments.

Says Investec Asset Management director Jeremy Gardiner to the Financial Mail August 2011, Many SA investors, having watched with horror over the past 10 years as the rand doubled in value and the JSE delivered enormous returns, are again considering switching at the wrong time — this time out of developed markets and into SA equities and the rand. “Yet again, this decision is made on the basis of emotional frustration rather than recognising that both SA equities and the rand are now relatively overvalued.”

But a steady hand is required here since the strong performance of the SA equity market seems set to continue. Offshore investment in general equities may well have dried up recently, it seems the JSE's R125bn listed property sector is becoming a hot commodity among overseas investors. Big institutions putting down their names include Principle Global Investors, Black Rock and State Street.

In 1997 the South African government allowed its citizens to take R200 000 per capita per annum to invest offshore. One may argue that investors practically ran to the offshore hills from an outperformed JSE and evaporating Rand. South African investors stood clutching their modest handful of Rands and looked up in wonder at a booming Wall Street. By 2001 the rand had fallen to R13.50 to the Dollar.

Who would believe that ten years later many countries would be on the verge of bankruptcy and that people would be grumbling about the “Strong Rand” and that the South African Equity market had outperformed most other markets over the same period?

But those in this game for the long haul will remind us that when all seems lost, it’s time to role up the sleeves and capitalise. Back in 2001 when fear gripped investors it was actually the right time to buy into SA equities. When the rand collapsed and afropessimism crept in, investors bought Dollars and Euros expensively and sold out of arguably undervalued markets and bought into markets trading at large premiums.

Looking back over ten years, comparisons have been made to a R100 investment in the JSE all-share index at the end of 2001 that would have been worth about R400 by the end of June this year, versus only around R94 if invested in the MSCI world index over the same period. The main US equity index, the S&P500, is today still roughly 10% below its peak in 2000 in rand terms. Emotions have been the main driver of the investments.

Says Investec Asset Management director Jeremy Gardiner to the Financial Mail August 2011, Many SA investors, having watched with horror over the past 10 years as the rand doubled in value and the JSE delivered enormous returns, are again considering switching at the wrong time — this time out of developed markets and into SA equities and the rand. “Yet again, this decision is made on the basis of emotional frustration rather than recognising that both SA equities and the rand are now relatively overvalued.”

But a steady hand is required here since the strong performance of the SA equity market seems set to continue. Offshore investment in general equities may well have dried up recently, it seems the JSE's R125bn listed property sector is becoming a hot commodity among overseas investors. Big institutions putting down their names include Principle Global Investors, Black Rock and State Street.

On the receiving end GrowthPoint properties, has seen its overseas shareholding jump from 3% to 11% a while back. Redefine - SA's second-biggest listed property counter, with a market cap of R20.3bn - doubled its offshore shareholding from 4% to 8% in the same period. “Global investors are now taking note of the fact South African-listed property offers far more attractive returns - total returns of close to 30% last year - than other global real estate markets.” Says Growthpoint executive director Estienne de Klerk.

There is expectation of more overseas funds showing up locally over the next 12 months. Names bandied about include Hyprop Investments, as well as what we've see materialise from the merger between Capital Property Fund and Pangbourne Properties, also whatever surfaces from the potential merger between Acucap Properties and Sycom Property Fund and then there’s the listing of Old Mutual's R12bn property portfolio.

Macquarie First South Securities property analyst Leon Allison spoke to Finance Week recently and said that although returns over the next decade will be more subdued than has been the case over the past 10 years, current positive structural changes will make the sector more investor-friendly.

Bringing us back to offshore options. The rand’s 'strength' favours taking money offshore. But the logic for offshore investment goes beyond any potential weakening of the rand. There is much to be said for the need for South Africans to diversify their assets. But there are more South Africans who have in the past got their offshore investment timing wrong. 2001 was the prime example, when a historic devaluing of the rand alarmed investors into the arms of foreign markets. At the peak of the rush, the second quarter 2001, 88% of net unit trust inflows went into offshore funds.

Now according to Marius Fenwick, head of the financial services arm of accountants Mazars: “Now is the opportune time to invest offshore as the strength of the rand makes offshore investment attractive. Instead, offshore diversification should be used to hedge future rand depreciation and diversify through access to large global companies.” So here we go again…

But we know already this isn’t all about the rand. The great Bismark said: “Some people learn from their mistakes, that’s good. But isn’t it better to learn from other people’s mistakes?” Aren’t the underperforming overseas markets just waiting for South African investors? Rand or no Rand variance?

What are the options? Who are the players in offshore property investment?

First of all there’s Growthpoint that bought up a Sydney listed subsidiary applying its winning formula in Australia. Then there’s Emira, which has just put R117m into Growthpoint Australia, in their case they claim the rand had zero to do with their investment move. Emira has a 6.4% stake in Growthpoint’s Australian presence.

International Property Solutions markets UK and Australian residential property to South African investors. CEO Scott Picken was quoted as saying that South Africans wait until the rand is collapsing, panic and throw their money into offshore apartments as it hits bottom, he says. “Most investors have lost money offshore in this decade.”

There is expectation of more overseas funds showing up locally over the next 12 months. Names bandied about include Hyprop Investments, as well as what we've see materialise from the merger between Capital Property Fund and Pangbourne Properties, also whatever surfaces from the potential merger between Acucap Properties and Sycom Property Fund and then there’s the listing of Old Mutual's R12bn property portfolio.

Macquarie First South Securities property analyst Leon Allison spoke to Finance Week recently and said that although returns over the next decade will be more subdued than has been the case over the past 10 years, current positive structural changes will make the sector more investor-friendly.

Bringing us back to offshore options. The rand’s 'strength' favours taking money offshore. But the logic for offshore investment goes beyond any potential weakening of the rand. There is much to be said for the need for South Africans to diversify their assets. But there are more South Africans who have in the past got their offshore investment timing wrong. 2001 was the prime example, when a historic devaluing of the rand alarmed investors into the arms of foreign markets. At the peak of the rush, the second quarter 2001, 88% of net unit trust inflows went into offshore funds.

Now according to Marius Fenwick, head of the financial services arm of accountants Mazars: “Now is the opportune time to invest offshore as the strength of the rand makes offshore investment attractive. Instead, offshore diversification should be used to hedge future rand depreciation and diversify through access to large global companies.” So here we go again…

But we know already this isn’t all about the rand. The great Bismark said: “Some people learn from their mistakes, that’s good. But isn’t it better to learn from other people’s mistakes?” Aren’t the underperforming overseas markets just waiting for South African investors? Rand or no Rand variance?

What are the options? Who are the players in offshore property investment?

First of all there’s Growthpoint that bought up a Sydney listed subsidiary applying its winning formula in Australia. Then there’s Emira, which has just put R117m into Growthpoint Australia, in their case they claim the rand had zero to do with their investment move. Emira has a 6.4% stake in Growthpoint’s Australian presence.

International Property Solutions markets UK and Australian residential property to South African investors. CEO Scott Picken was quoted as saying that South Africans wait until the rand is collapsing, panic and throw their money into offshore apartments as it hits bottom, he says. “Most investors have lost money offshore in this decade.”

Financial correspondent Scott Picken writes that comparative data shows that South Africans would have made much more money over 10 years measured in sterling by buying an average house in Johannesburg in 1997 than buying one in London at the same time. Only time will tell if the shoe is now on the other foot.

Other off shore institutional investors include Capital Shopping Centres. British Capital, run through Barnard Jacobs Mellet and Stanlib which has offshore unit trusts. Investec Property Investments has unlisted funds buying property in Europe and the US. There is also Catalyst which has an unlisted fund of global listed property funds. Redefine is working through its London-listed Redefine International. Resilient has New Europe Property Investments (Nepi), which mainly owns shopping centres in Romania. All top performers.

Other choices in property include these very few funds which have actually lost money. Nedgroup Global Cautious (down 8,5%); Sanlam Investment Management Global Best Ideas (down 2,3%) a long term performer though; the Absa International fund of funds (down 15,8%)

Whether it’s a strong Rand or the need to diversify one’s portfolio, these may be the times that offshore property funds offer the South African investor a long term strategy again, last made available ten years ago. Whatever the case this isn’t the time to think with the knee-jerk of emotion or a political bias.

Other off shore institutional investors include Capital Shopping Centres. British Capital, run through Barnard Jacobs Mellet and Stanlib which has offshore unit trusts. Investec Property Investments has unlisted funds buying property in Europe and the US. There is also Catalyst which has an unlisted fund of global listed property funds. Redefine is working through its London-listed Redefine International. Resilient has New Europe Property Investments (Nepi), which mainly owns shopping centres in Romania. All top performers.

Other choices in property include these very few funds which have actually lost money. Nedgroup Global Cautious (down 8,5%); Sanlam Investment Management Global Best Ideas (down 2,3%) a long term performer though; the Absa International fund of funds (down 15,8%)

Whether it’s a strong Rand or the need to diversify one’s portfolio, these may be the times that offshore property funds offer the South African investor a long term strategy again, last made available ten years ago. Whatever the case this isn’t the time to think with the knee-jerk of emotion or a political bias.

For more articles by Matthew Campaigne-Scott Click Here